Society & Governance

Public Debt, Taxation & Fiscal Credibility

TopicFR

Not whether France taxes heavily, but whether it can fund its social model credibly—through fair design, medium-term rules, and reforms citizens, EU institutions, and markets will believe.

Last reviewed 2026-05-31 · updated against official and high-quality sources

OAP view

France's fiscal problem is not solved by symbolic battles over the ISF, by unpaid payroll cuts, or by pretending the social model can continue without consolidation. The durable path is hybrid credibility: protect investment and universal floors, review spending and tax expenditures honestly, reduce the labour wedge where it most hurts hiring, finance relief transparently, price carbon only with visible rebates, and publish medium-term fiscal paths the Haut Conseil des Finances Publiques, EU institutions, citizens, and markets can audit.

Thesis

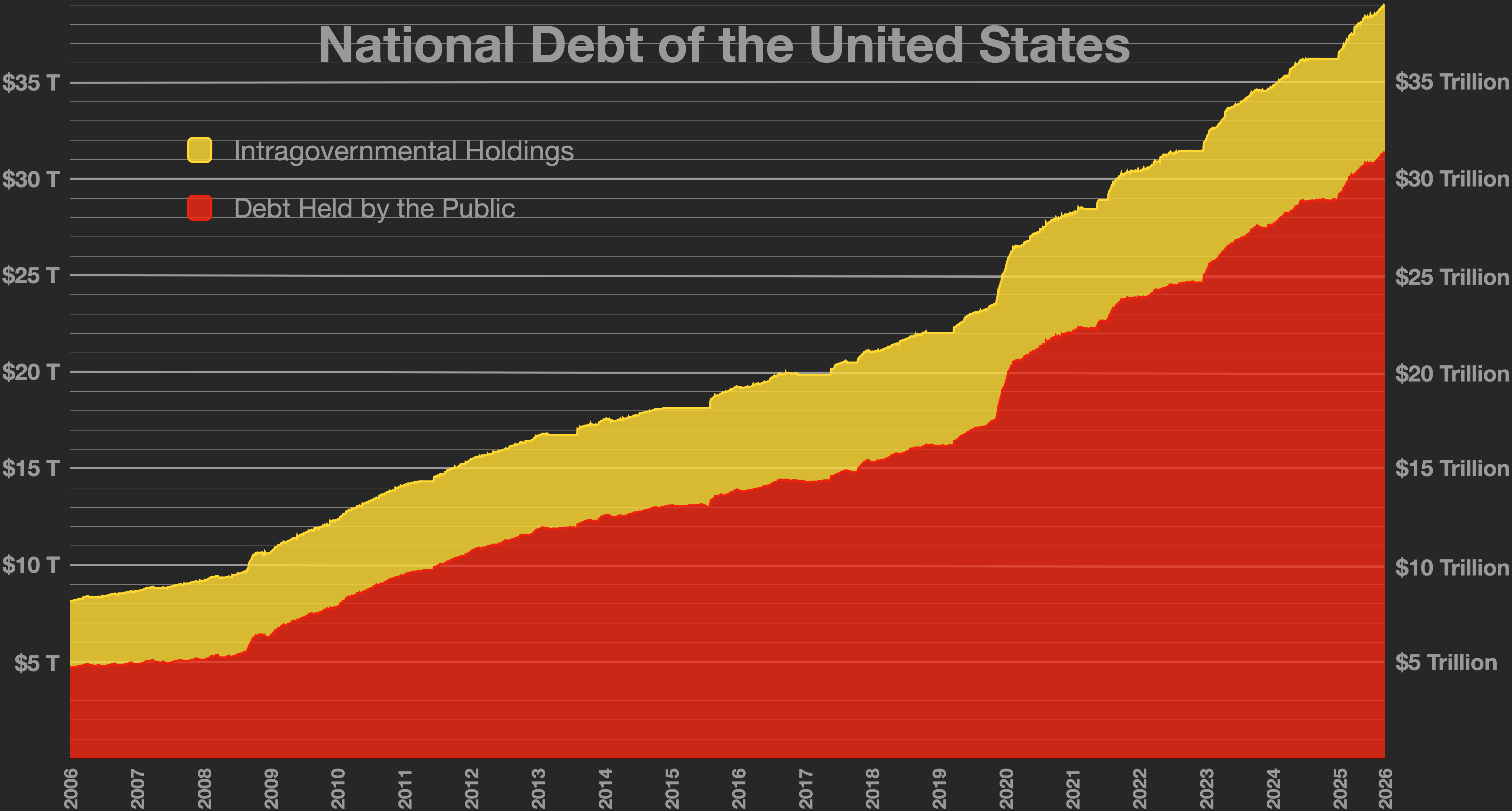

France runs one of Europe's highest tax-and-social-contribution regimes to fund pensions, healthcare, education, public employment, and social protection. That model bought stability for decades, but the latest fiscal data show a binding credibility problem: INSEE put the 2025 public deficit at 5.1% of GDP, after 5.8% in 2024, and Maastricht public debt at 115.6% of GDP at the end of 2025.

A serious policy must do three things at once: stabilize debt without crushing growth, redesign who pays—labour, capital, consumption, property, carbon—in ways voters experience as fair, and rebuild budget institutions so fiscal choices are programmed rather than improvised after each parliamentary crisis.

The visible debate is taxes versus austerity. The deeper debate is whether the French state can still deliver on its promises while financing them transparently.

Key numbers

Live civic-intelligence dashboard — judge integration by measurable performance, not posture.

- Public debtHigh confidence115.6% of GDP at end-2025113.0% of GDP at end-2024; 115.6% at end-2025This replaces the older '~110%' shorthand; net debt was lower at 108.4% of GDP, but Maastricht gross debt is the EU headline measure.Source: INSEE, Maastricht debt Q4 2025· Verified 2026-05-31

- Public deficitHigh confidence5.1% of GDP in 20255.4% in 2023; 5.8% in 2024; 5.1% in 2025Still well above the EU 3% reference value and above the debt-stabilising level.Source: INSEE national accounts, 2025· Verified 2026-05-31

- Tax-to-GDP ratioHigh confidence43.5% in 2024OECD preliminary 2024 cross-country dataOECD reports France had the second-highest tax-to-GDP ratio in 2024, after Denmark.Source: OECD Revenue Statistics 2025· Verified 2026-05-31

- Compulsory-tax rateHigh confidence43.6% of GDP in 20252024–2025INSEE's compulsory-tax-rate concept differs from the OECD tax-to-GDP series, but both confirm France remains a high-levy state.Source: INSEE 2025 public finances· Verified 2026-05-31

- Labour tax wedgeHigh confidence47.2% for a single average worker in 202547.1% in 2024; OECD average 35.1% in 2025Core competitiveness and take-home-pay constraint; France ranked third-highest among OECD members in 2025 for this measure.Source: OECD Taxing Wages 2026, France note· Verified 2026-05-31

- Public expenditureHigh confidence57.2% of GDP in 202557.0% in 2024; 57.2% in 2025The fiscal issue is not low revenue; it is the interaction of high spending, high levies, slow growth, and political resistance to credible consolidation.Source: INSEE 2025 public finances· Verified 2026-05-31

- Pension age pathMedium confidence64 target under 2023 reform; implementation politically suspended/contested2023 reform; 2025–2027 suspension debateDo not display simply as '64 stable'; the 64 target remains the reform reference, but implementation has been politically suspended/contested pending later decisions.Source: Service-public.fr and 2025 parliamentary reporting· Verified 2026-05-31

- Corporate tax headline rateHigh confidence25% standard rateFinancial years commencing on or after 1 Jan. 2022Effective burdens vary through credits, sector rules, surcharges, and temporary exceptional contributions.Source: impots.gouv.fr / French tax code· Verified 2026-05-31

Definitions

Immigration debates mix categories. These terms are used consistently on this page.

- Cotisations sociales

- Employer and employee social contributions funding pensions, health, family, and unemployment schemes—often heavier than income tax on labor.

- ISF / IFI

- The wealth tax (ISF) was abolished in 2018; IFI (impôt sur la fortune immobilière) now taxes real-estate wealth above thresholds, not financial portfolios.

- PFU (flat tax)

- Prélèvement forfaitaire unique: 30% on many capital incomes (12.8% income tax + 17.2% social levies), with optional progressive schedule.

- CSG / CRDS

- Generalized social contribution and debt-repayment contribution applied to wages, pensions, and capital income.

- Impôt sur les sociétés (IS)

- Corporate income tax; headline rate reduced toward 25% with R&D and manufacturing incentives, but effective rates vary by firm.

- Loi de finances / loi de programmation

- Annual budget law and multi-year fiscal programming act—credibility depends on both being coherent and durable.

At a glance

- 01

Scale

France combines very high public spending with very high tax and social charges. Maastricht debt reached 115.6% of GDP at end-2025 and the deficit was 5.1% of GDP in 2025.

- 02

Direction of travel

The deficit narrowed from 5.8% in 2024 to 5.1% in 2025, but debt still rose and remains far above the euro-area average; political fragmentation makes consolidation harder.

- 03

Why now

France is under an ongoing EU excessive-deficit procedure, interest costs are more salient, and fragmented parliaments turn annual budgets into legitimacy tests.

- 04

What success should mean

A credible medium-term path, fair tax design, protected investment floors, pension transparency, lower labour wedges where they most damage hiring, and carbon policy that does not recreate Gilets Jaunes dynamics.

Tax and levy instruments

French fiscal stress is not one tax. Payroll charges, income tax, wealth and property levies, corporate tax, VAT, and carbon pricing each create different winners, losers, and reform paths.

Payroll & cotisations

- Scale

- Largest perceived burden on work and hiring

- Policy problem

- High employer charges depress jobs and wages; cuts need replacement revenue

OAP note Any payroll relief must be scored against PFU, IFI, VAT, or spending.

Income tax & PFU

- Scale

- Progressive IR on wages; flat 30% option on capital

- Policy problem

- Perceived unfairness between labor and portfolio income

OAP note PFU narrowing is politically easier than full ISF restoration for many.

Wealth & property (IFI)

- Scale

- Targets real estate holdings above thresholds

- Policy problem

- Does not reach financial wealth; symbolically charged

OAP note Expansion vs payroll tradeoff is the live left-right axis.

VAT & consumption

- Scale

- Major revenue base with regressive edges

- Policy problem

- Raising VAT hits purchasing power; Gilets Jaunes memory

OAP note Often used to finance payroll cuts in European packages.

Corporate tax (IS)

- Scale

- Headline 25% with credits and sector rules

- Policy problem

- Effective rates and compliance differ sharply by firm size

OAP note Condition credits on hiring and decarbonization, not rent-seeking.

Carbon & energy levies

- Scale

- Domestic carbon path + EU ETS + fuel duties

- Policy problem

- Climate credibility vs rural and low-income backlash

OAP note Rebates are part of design, not an afterthought.

Data · Debt, deficit, and EU frame

| Signal | Latest useful figure | Why it matters |

|---|---|---|

| Maastricht public debt | 115.6% of GDP at end-2025 | The headline EU debt measure and the anchor for market and Brussels scrutiny. |

| Public deficit | 5.1% of GDP in 2025 | Improved from 2024 but still well above the EU 3% reference value. |

| Ongoing excessive-deficit procedure | Procedure opened in 2024; Council recommendation in 2025 | Fiscal discretion is now bounded by EU monitoring and market credibility. |

| Euro-area comparison | Euro-area debt 87.8% of GDP at end-2025 | France’s debt ratio is well above the euro-area aggregate. |

Data · Tax structure and reform pressure

| Signal | Latest useful figure | Why it matters |

|---|---|---|

| OECD tax-to-GDP ratio | 43.5% in 2024 | France is already one of the highest-tax OECD countries; credibility cannot come only from raising headline rates. |

| Compulsory-tax rate | 43.6% of GDP in 2025 | INSEE’s 2025 measure rose from 42.8% in 2024, showing revenues improved but not enough to close the gap. |

| Labour tax wedge | 47.2% in 2025 for a single average worker | The labour wedge is central to hiring, take-home pay, and competitiveness. |

| Corporate income tax | 25% standard rate | France lowered the headline rate, but effective burdens and temporary surcharges still matter. |

Data · Major reform milestones

| Signal | Latest useful figure | Why it matters |

|---|---|---|

| ISF abolished → IFI | 2018 | Shifted wealth taxation toward property only and remains a symbolic fairness fault line. |

| PFU on capital income | 30% flat option | Central to fairness debate between labour and portfolio income. |

| Pension reform | 64 target, but implementation suspended/contested | Largest contested consolidation lever; do not treat as politically settled. |

| Taxe d'habitation on primary homes | Phased out nationally | Popular national cut; shifted local-finance pressure elsewhere. |

EU rules and market constraints

France does not have an asylum-style fiscal problem; this field is reused by the UI to show EU rules and market constraints. The relevant constraint is euro-area fiscal discipline: France is under an excessive-deficit procedure, public debt reached 115.6% of GDP at end-2025, and the deficit remained 5.1% of GDP in 2025. The revised EU framework relies on medium-term plans and country-specific adjustment paths, while markets price political credibility through spreads when budget processes stall.

| Signal | Figure / metric | Why it matters |

|---|---|---|

| Haut Conseil des Finances Publiques (HCFP) | Independent assessment of macro and fiscal assumptions | Credibility requires budget plans that survive independent scrutiny. |

| EU excessive-deficit procedure | Ongoing for France | The deficit path is now formally monitored under EU rules. |

| Interest expenditure | Rising salience as debt stock grows | Higher debt service can crowd out investment and social floors. |

Capacity pressures

- Fragmented parliament and repeated budget-confidence dynamics

- Pension and healthcare demographics

- High public spending at 57.2% of GDP in 2025

- Energy transition, defence, and industrial-policy investment needs

- Symbolic tax fights that avoid base-broadening and spending review

Policy directionPublish a credible loi de programmation pluriannuelle, align EU green/industrial envelopes with national financing choices, and stop treating annual budget crises as substitutes for multi-year tradeoffs.

What is really at stake

The visible debate

Tax the rich versus protect the social model; cut deficits versus avoid austerity; restore ISF versus cut payroll charges.

The deeper debate

Whether France can maintain universal services and EU leadership while rebalancing who pays and making the state deliver on its promises.

The institutional test

Can the republic pass and stick to medium-term fiscal law when every budget becomes a confidence vote?

Core fault lines

Payroll vs capital

Cotisations and charges patronales versus PFU/IFI and portfolio income.

OAP view

Fairness requires moving the wedge, not only debating symbols.

Carbon vs purchasing power

Climate pricing against Gilets Jaunes memory and rural car dependence.

OAP view

Explicit rebates and rural mobility credits are part of credible design.

EU rules vs French discretion

Brussels trajectories versus national choices on investment and social floors.

OAP view

Use EU frameworks; do not hide distributional choices inside Brussels.

Consolidation vs public employment

Spending reviews touch hospitals, schools, prefectures, and local states.

OAP view

Attrition and efficiency before blanket service collapse narratives.

Fiscal outcomes to track

Entry numbers matter less than what happens after arrival — employment, schools, housing, discrimination, and trust.

Debt path credibility

Stable or falling debt/GDP over 5–7 years

What this meansMarkets and EU stop pricing French risk as idiosyncratic.

Success metricPublished trajectory with HCFP endorsement

Payroll wedge reduction

Lower employer charges on low/median wages

What this meansHiring and take-home pay improve without revenue collapse.

Success metricScored package vs PFU/IFI/VAT adjustments

Pension sustainability

Parametric reforms plus demographic transparency

What this means49.3-style passage is not repeated every decade.

Success metricIndependent scoring and phased implementation

Carbon legitimacy

Price path + visible rebates

What this meansEcological tax is not default-regressive.

Success metricRural and low-income compensation tracked publicly

Bottlenecks

Assemblée nationale (fragmented)

StrainBudgets become confidence votes; medium-term law stalls

Reform directionCoalition contracts on programming, not only annual survival

Ministry of Finance / Bercy

StrainExpedient measures vs structural base reform

Reform directionPublish tax-expenditure and subsidy reviews with parliament

HCFP

StrainWarnings ignored in campaign seasons

Reform directionBind loi de programmation to HCFP scenarios

Local governments

StrainHabitation cuts shifted revenue stress

Reform directionTransparent local finance reform, not unfunded mandates

Current signals

- 1

2025 deficit improved but remains excessive

INSEE puts the deficit at 5.1% of GDP in 2025 after 5.8% in 2024; improvement is real but not yet debt-stabilising.

- 2

Debt ratio rose to a new credibility level

Maastricht public debt reached 115.6% of GDP at end-2025, far above the euro-area aggregate.

- 3

Pension reform is not politically settled

The 64 target remains the reform reference, but implementation has been suspended/contested in the 2025–2027 political cycle.

- 4

Labour taxation remains a binding constraint

The OECD puts France’s 2025 single-worker tax wedge at 47.2%, the third-highest among OECD members.

- 5

EU oversight is active

France remains under an excessive-deficit procedure, so domestic budget design is judged against EU adjustment expectations.

Policy options

Compare approaches by upside, risk, and who bears the cost — not by slogan.

| Option | Upside | Risk | Who benefits | Who bears cost | OAP assessment |

|---|---|---|---|---|---|

| Austerity-only consolidation | Fast deficit reduction on paper | Growth hit, protest, service collapse narratives | Bondholders short-term | Middle incomes and regions dependent on public jobs | Reject as sole strategy. |

| Restore broad ISF without payroll reform | Symbolic fairness on wealth | Capital flight narratives; employment unchanged | Progressive coalitions | Investors and mobile professionals (per debate) | Incomplete unless paired with labor wedge relief. |

| Payroll cuts without revenue replacement | Short-term competitiveness signal | Deficit blowout; EU and market stress | Employers | Future taxpayers and service users | Reject unless scored against PFU/IFI/VAT/spending. |

| Hybrid credibility package (OAP preferred) | Balances consolidation, fairness, investment, and EU alignment | Requires coalition discipline and administrative follow-through | Workers, investors seeking stability, EU partners | Actors profiting from fiscal chaos politics | Preferred: medium-term programming plus targeted tax and spending design. |

Who opposes this

A serious package must name resistance—not pretend consensus exists.

Unions and street mobilization

Likely objectionReforms are illegitimate and regressive.

OAP response

Process and rebate design matter; parametric pension and payroll shifts need independent scoring and phased timelines.

Business federations

Likely objectionCharges patronales still too high.

OAP response

Agree on wedge reduction if anti-evasion and SME simplification are real, not cosmetic.

Wealth-tax advocates

Likely objectionPFU and IFI are unfair.

OAP response

Expand property and reporting integrity before symbolic rates; pair with payroll relief for median earners.

Brussels and bond markets

Likely objectionPlans are not credible or durable.

OAP response

Loi de programmation plus HCFP visibility beats annual crisis management.

OAP package

Hybrid fiscal credibility

Not ISF theatre. Not austerity alone. Not unpaid payroll cuts.

France should fund its social model with published medium-term paths, payroll relief financed fairly, protected investment floors, carbon pricing with rebates, and spending reviews that target subsidies and tax expenditures before universal services.

- 1

Medium-term programming

Main blockerFragmented Assemblée and short-lived governments.

Bind annual loi de finances to a published pluriannual path.

- Loi de programmation with HCFP scenarios

- Debt and deficit ceilings with escape clauses for verified investment

- Public dashboard on interest and pension costs

- 2

Payroll relief with fair financing

Main blockerRevenue replacement politics.

Cut employer cotisations on low and median wages.

- Targeted employer charge cuts

- PFU narrowing on highest capital incomes

- IFI reporting integrity and anti-evasion on platforms and corporates

- 3

Pension parametrics with legitimacy

Main blockerUnion mobilization and retirement-age symbolism.

Keep demographic scoring public; avoid repeated 49.3 surprises.

- Independent pension council publications

- Indexation and special-regime reviews

- Phased implementation with regional impact data

- 4

Carbon price + rebates

Main blockerGilets Jaunes memory and rural dependence on cars.

Make ecological tax visibly non-regressive by default.

- Explicit carbon-price path

- Household and rural mobility credits

- Track rebate uptake by income decile and region

- 5

Spending and tax-expenditure review

Main blockerSectoral lobbies and public-employment politics.

Measureable cuts in subsidies and niches before universal service erosion.

- Published tax-expenditure inventory

- Subsidy sunset clauses

- Public employment attrition where digitalization allows

Not this

- Annual budget chaos without programming

- Payroll cuts with no revenue score

- ISF restoration with no labor-wedge plan

- Carbon prices without rebates

- Deferring pension and interest honesty

OAP working view

France should move from symbolic tax fights to fiscal credibility politics.

Judge success by debt trajectory, deficit reduction, OAT spread stability, labour-tax wedge on median workers, pension-scheme transparency, carbon-price legitimacy outside Paris, and whether HCFP assessments are acted on. The strongest approach is hybrid consolidation: fair tax design, protected investment and social floors, labour-cost relief where it improves employment, and institutions that program rather than improvise.

The central failure mode is treating fiscal reform as culture war—ISF versus Macron, austerity versus generosity—instead of building executable packages that markets and citizens can track.

Policy performance dashboard

What good looks like vs failure mode — by policy area.

| Policy area | What good would look like | Failure mode |

|---|---|---|

| Medium-term fiscal law | Published loi de programmation with HCFP alignment | Annual crisis budgets and spread spikes |

| Payroll taxation | Lower wedge on low/median wages, scored financing | Unfunded cuts or no hiring response |

| Pensions | Transparent demographics and phased parametrics | Repeated 49.3 legitimacy crises |

| Carbon pricing | Price path plus visible rebates | Gilets Jaunes-style backlash |

| Corporate tax | Stable IS with SME simplification and conditioned credits | Rent-seeking and effective-rate dispersion |

What we would watch next

- 1

OAT spreads vs Germany

Early signal when budget negotiations stall.

- 2

HCFP opinions on draft budgets

Whether warnings are incorporated or ignored.

- 3

Loi de finances adoption timeline

Expedients and continuances signal institutional stress.

- 4

Payroll reform proposals

Watch financing sources named alongside cotisation cuts.

- 5

Carbon rebate uptake

Regional and income breakdown reveals legitimacy.

Mind changers

Specific measurable indicators — not vibes.

More optimistic if

- Multi-year fiscal law passes with cross-bench elements

- Debt/GDP stabilizes while investment floors hold

- Employer charges fall on median wages without deficit blowout

- Carbon rebates reduce net burden on rural low incomes

More pessimistic if

- Repeated no-confidence cycles without programming

- Spread stress returns during budget deadlocks

- Payroll cuts announced without revenue score

- Pension or carbon fights displace base-broadening

OAP scorecard

- Fiscal credibility4/10

The 2025 deficit improved to 5.1% of GDP, but debt reached 115.6% of GDP and politics remain fragmented.

- Evidence confidence9/10

INSEE, OECD, Eurostat, the European Commission, and HCFP provide strong public data for debt, deficit, tax and wage-burden measures.

- Political temperature9/10

Pensions, wealth-tax symbolism, high levies, budget votes, and hung-parliament dynamics keep fiscal politics hot.

- Institutional stress8/10

The budget process, EU procedure, local finance, pension settlement, and delivery capacity are all under pressure.

- Policy solvability6/10

Technically coherent hybrid packages are available, but they require coalition discipline and trusted implementation.

- Performance-measurement readiness8/10

France has excellent public fiscal data; the gap is not data availability but political uptake and public-facing dashboards.

Sources

Official statistics, EU institutions, and selected expert analysis used for this profile.

- INSEE — 2025 public deficit and public finances

- INSEE — Q4 2025 Maastricht debt

- Eurostat — euro-area debt and deficit 2025

- European Commission — Excessive Deficit Procedure: France

- OECD — Revenue Statistics 2025 tax-to-GDP trends

- OECD — Taxing Wages 2026 France country note

- Service-public.fr — retirement age and reform timetable

- impots.gouv.fr — corporate tax standard rate

- HCFP — 2026 budget opinion

Related articles

Recent reporting tagged to this topic—read snapshots first, then open full analyses.